Baby Boomers Are Loaded Why So Stingy?

Baby boomers are loaded why are they so stingy – Baby Boomers Are Loaded: Why So Stingy? It’s a question that pops up in conversations, online forums, and even family dinners. Are the stereotypes true? Are Boomers really sitting on mountains of cash, hoarding their wealth while younger generations struggle? This isn’t just about generational differences; it’s about understanding the historical context that shaped their financial habits, the pressures they faced, and how their experiences continue to influence their spending today.

Let’s dive into the complexities behind this intriguing question.

We’ll explore how events like the Great Depression and the post-war era instilled a deep-seated frugality in this generation. We’ll also examine how their financial priorities shifted throughout different life stages – from raising families and paying for college to navigating retirement. Comparing their wealth accumulation strategies with those of Millennials and Gen X will help us understand the perceived differences in spending habits.

Finally, we’ll unpack the role of societal perceptions, media portrayals, and charitable giving in shaping the narrative surrounding Baby Boomer finances.

The Great Depression and Post-War Frugality

The stereotype of the frugal Baby Boomer isn’t entirely unfounded. Their formative years were profoundly shaped by economic hardship and societal shifts that instilled a deep-seated value on saving and careful spending, a legacy that continues to influence their financial behaviors today. Understanding their experiences provides crucial context for interpreting their current financial attitudes.The Great Depression, lasting from 1929 to the late 1930s, cast a long shadow over the lives of Baby Boomers, even those born after its official end.

Their parents and grandparents lived through widespread unemployment, poverty, and food scarcity. Witnessing this level of economic instability instilled a profound fear of financial insecurity that permeated subsequent generations. This wasn’t simply a matter of learning about hardship; it was a lived experience, shaping their worldview and financial priorities in profound ways. The stories of belt-tightening, resourcefulness, and careful budgeting were not abstract lessons but the very fabric of their childhoods.

The Impact of Post-War Societal Values

Post-World War II saw a period of unprecedented economic growth in the United States. However, the values of frugality and self-reliance forged during the Depression remained strong. The post-war era, while prosperous, also emphasized hard work, delayed gratification, and financial responsibility. Homeownership became a symbol of success, but it was often achieved through diligent saving and careful planning, reflecting the cautious approach ingrained by the Depression.

This contrasted with the consumerism that began to rise later in the century, and Boomers often maintained a more conservative approach to spending compared to later generations.

Economic Realities: Then and Now

The economic realities of Baby Boomers’ youth were vastly different from today’s. They experienced a time of relatively low inflation, readily available jobs (though often in less lucrative sectors initially), and a greater emphasis on job security. While the post-war era saw rising prosperity, it was built on a foundation of careful budgeting and thriftiness. Contrast this with the current environment of fluctuating inflation, the gig economy, and increasing student loan debt.

The relative stability of the post-war era, coupled with the lessons of the Depression, fostered a mindset that prioritized saving and minimizing debt. This is a significant factor in understanding the perceived “stinginess” attributed to this generation.

Examples of Frugality

The impact of these experiences is evident in various aspects of Baby Boomers’ financial behavior. For example, many prioritized paying off their mortgages early, avoiding unnecessary debt, and diligently saving for retirement. They often repaired items instead of replacing them, passed down clothing and toys, and generally practiced a more resourceful approach to consumption. This isn’t necessarily about being stingy; it’s a reflection of deeply ingrained values shaped by the unique economic and social context of their lives.

Okay, so Baby Boomers are loaded, right? But why the tightfisted reputation? Maybe it’s a generational thing, a learned behavior from a time of scarcity. Or perhaps it’s like exploring the worlds most studied rainforest is still yielding new insights – even after years of study, there are still surprises. Similarly, maybe there are still untold aspects to Boomer financial behavior that we haven’t uncovered yet.

Maybe they’re just saving for something we can’t quite fathom.

These practices, though perhaps viewed as outdated by some, represent a legacy of resilience and financial prudence.

Different Stages of Life and Financial Priorities

Baby Boomers, born between 1946 and 1964, experienced a dramatically shifting economic landscape throughout their lives. Understanding their financial priorities across different life stages helps explain some of their saving and spending behaviors. Their experiences shaped their approach to money, often leading to a more cautious and conservative financial outlook compared to some subsequent generations.

Financial priorities are not static; they evolve significantly as individuals progress through various life stages. For Baby Boomers, these shifts were particularly pronounced, influenced by factors like the post-war economic boom, the rise of consumerism, and the increasing costs of higher education and healthcare.

Financial Priorities During Early Adulthood (20s-30s), Baby boomers are loaded why are they so stingy

During their early adulthood, many Baby Boomers focused on establishing careers and families. Major expenses included securing housing (often purchasing a home), starting a family, and paying off student loans (though significantly less prevalent than in later generations). Saving goals primarily revolved around building an emergency fund and making down payments on houses. Spending habits often leaned towards building a comfortable home life and providing for young children, sometimes prioritizing immediate needs over long-term savings.

Many Boomers experienced relatively rapid economic growth, making homeownership a more achievable goal than it is for some younger generations today.

Financial Priorities During Middle Age (40s-50s)

This period often brought increased financial responsibilities. The major expenses included raising children, paying for their education (college tuition costs were a significant burden for many), and maintaining a household. Saving goals expanded to include retirement planning, paying off mortgages, and potentially funding children’s education. Spending habits often reflected the competing needs of raising a family and saving for the future, resulting in a careful balancing act between immediate needs and long-term financial security.

Many Boomers experienced peak earning years during this time, allowing for more substantial savings and investments.

Financial Priorities During Retirement (60s and beyond)

Retirement presented a new set of financial priorities. Major expenses shifted to healthcare costs (which have risen dramatically), housing, and leisure activities. Saving goals focused on maintaining a comfortable retirement lifestyle and covering unexpected medical expenses. Spending habits often reflected a desire to enjoy retirement, but also a need to carefully manage resources to ensure financial security for the remainder of their lives.

Okay, so Baby Boomers are famously loaded, right? But why the tightfistedness? It makes you wonder about priorities, you know? I mean, reading about the incredible work towards religious harmony happening in a place like the hopes for religious harmony come to life in the muslim vatican , makes you think about how resources could be used to foster such positive change.

Maybe that’s a key to understanding why some Boomers seem to hoard their wealth – a different set of values entirely.

The reality of healthcare costs and potential longevity often led to a more conservative spending approach in retirement than many had anticipated.

| Life Stage | Major Expenses | Saving Goals | Spending Habits |

|---|---|---|---|

| Early Adulthood (20s-30s) | Housing, starting a family, student loans | Emergency fund, down payment on house | Building a home, providing for young children |

| Middle Age (40s-50s) | Raising children, college tuition, home maintenance | Retirement planning, mortgage payoff, children’s education | Balancing family needs and long-term savings |

| Retirement (60s and beyond) | Healthcare, housing, leisure activities | Maintaining retirement lifestyle, covering medical expenses | Careful management of resources |

Wealth Distribution and Generational Differences

The perception of Baby Boomers as stingy often overshadows a complex reality regarding wealth distribution across generations. While some Boomers may exhibit frugal habits, a significant portion accumulated considerable wealth during their working lives, creating a notable generational wealth gap. Understanding the factors behind this disparity requires examining the economic landscape they navigated and comparing their financial strategies to those of subsequent generations.Factors contributing to Baby Boomer wealth accumulation are multifaceted.

Many benefited from a robust post-war economy with ample job opportunities and rising wages. Homeownership became increasingly attainable, and real estate values appreciated significantly, building substantial equity. Furthermore, many Boomers enjoyed employer-sponsored pension plans and defined benefit retirement schemes, providing a guaranteed income stream in retirement, unlike many younger generations. These factors, combined with longer working careers and often lower student loan debt compared to Millennials, contributed to their higher net worth.

Comparison of Wealth Accumulation Strategies

Baby Boomers generally prioritized long-term investments, often focusing on stable assets like real estate and company stock. Their approach was often characterized by patience and a long-term perspective. In contrast, Millennials and Gen X faced different economic realities. Higher education costs, stagnant wages, and the Great Recession significantly impacted their ability to save and invest aggressively. They are more likely to utilize diverse investment strategies, including index funds and actively managed portfolios, reflecting a greater emphasis on diversification and potentially higher risk tolerance due to a longer time horizon until retirement.

Okay, so baby boomers are loaded, right? But why the tightfistedness? Maybe it’s because they witnessed economic uncertainty, unlike today’s seemingly more carefree generations. I was reading this fascinating article on can china smash the airbus boeing duopoly , and it got me thinking about how different generations handle wealth and risk. Perhaps the boomers’ frugality stems from a deep-seated need for security, a lesson learned during their formative years.

Gen X, caught between the relatively stable economic climate of the Boomers and the challenging circumstances of Millennials, often adopted a mix of both strategies, attempting to balance risk and security.

Reasons for Perceived Differences in Spending Habits

The perceived differences in spending habits between generations are not solely about frugality. Boomers often benefited from lower living costs, particularly in housing and healthcare, during their peak earning years. Their retirement plans, while not universally successful, offered a degree of financial security that younger generations often lack. This financial security, coupled with the accumulation of assets over decades, allows many Boomers more discretionary spending capacity, even if their spending patterns appear conservative compared to younger generations’ more digitally driven consumption habits.

Millennials and Gen X, facing higher living costs and greater financial uncertainty, may prioritize immediate needs over long-term savings.

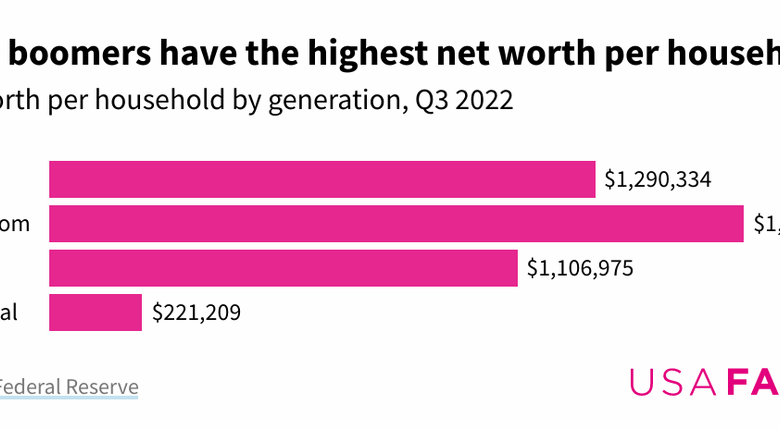

Visual Representation of Generational Net Worth

Imagine a bar graph depicting the average net worth of different generations. The bar representing Baby Boomers would be significantly taller than those representing Gen X and Millennials. The height difference would visually represent the substantial wealth gap. The graph could further break down net worth by asset class (e.g., real estate, retirement accounts, investments) to illustrate the composition of wealth across generations and highlight the impact of factors such as homeownership and pension plans on the overall wealth distribution.

The visual would clearly demonstrate the significant disparity in average net worth, underscoring the complex interplay of economic factors and generational experiences in shaping wealth accumulation.

Perceptions of Wealth and Generational Stereotypes

The stereotype of the frugal Baby Boomer is deeply ingrained in popular culture, often overshadowing the diverse financial realities of this generation. This perception, fueled by societal narratives and media portrayals, significantly impacts how Baby Boomers are viewed and, perhaps more importantly, how they view themselves and their spending habits. Understanding the nuances of this perception is crucial to separating fact from fiction.Societal perceptions of wealth and spending heavily influence individual behavior, creating a feedback loop that reinforces existing stereotypes.

For instance, the prevailing societal message that equates material possessions with success can pressure individuals, regardless of their generation, to conform to certain spending patterns. Conversely, a culture that values frugality and saving can lead to different behavioral choices. This cultural context shapes how individuals perceive their own financial situations and their spending choices.

The Impact of Negative Stereotypes on Baby Boomers

Negative stereotypes associated with Baby Boomers’ frugality can have a significant psychological and social impact. Being labeled “stingy” or “cheap” can be hurtful and isolating, leading to feelings of inadequacy or shame. This can affect their relationships with family and friends, particularly younger generations who may struggle to understand their financial priorities. Furthermore, these stereotypes can prevent open and honest conversations about finances within families, hindering financial planning and support.

The constant pressure to conform to societal expectations of spending can create internal conflict, especially for Boomers who value financial security above all else. This conflict can manifest in feelings of guilt or anxiety related to spending, even when financially justified.

Media Portrayals and the Reinforcement of Stereotypes

Media portrayals often contribute significantly to the perpetuation of these stereotypes. Sitcoms, movies, and even news articles frequently depict Baby Boomers as penny-pinching individuals, clinging to outdated ideas about money management. These portrayals, while sometimes comedic, can solidify negative stereotypes in the public consciousness. For example, a common trope shows a Baby Boomer character meticulously clipping coupons or haggling aggressively over small amounts of money, reinforcing the image of them as excessively frugal.

This portrayal is often done for comedic effect, but the cumulative impact reinforces a negative stereotype. Another example is the depiction of Baby Boomers struggling to adapt to new technologies, implying a lack of willingness to spend on modern conveniences, furthering the “stingy” image.

Comparing Perceptions with Reality: The Financial Situation of Baby Boomers

The reality of Baby Boomers’ financial situations is far more complex than the simplified narrative of universal frugality suggests. While many Boomers did experience periods of economic hardship, such as the Great Depression or post-war rationing, many also experienced significant economic growth and benefited from robust job markets. The financial well-being of Baby Boomers varies greatly depending on factors like career choices, educational attainment, health, and investment strategies.

While some have accumulated substantial wealth, others face financial insecurity in retirement, struggling with healthcare costs and fixed incomes. Therefore, it is inaccurate to characterize the entire generation with a single, simplistic label. The wide range of financial situations within the Baby Boomer generation highlights the danger of applying broad generalizations based solely on stereotypes. Many Boomers prioritized saving and investing for the future, a strategy that might appear “stingy” to those who prioritize immediate gratification but ultimately provided financial security in their later years.

Philanthropy and Charitable Giving Among Baby Boomers: Baby Boomers Are Loaded Why Are They So Stingy

The stereotype of Baby Boomers as stingy often overshadows their significant contributions to philanthropy and charitable giving. While fiscal conservatism born from experiences like the Great Depression and a focus on building personal wealth are undeniable factors, a closer look reveals a substantial level of charitable engagement among this generation. Their giving, however, often takes different forms and is driven by motivations distinct from younger generations.Baby Boomers’ philanthropic activities significantly impact the perception of their financial habits.

Large-scale donations and consistent support of various causes actively counter the “stingy” narrative. This active engagement in giving demonstrates a commitment to societal well-being that transcends personal financial accumulation. The sheer volume of charitable giving by this generation, even if spread across numerous smaller donations, is considerable and contributes significantly to the non-profit sector.

Motivations Behind Baby Boomer Charitable Giving

Baby Boomers’ charitable giving is often motivated by a deep-seated sense of social responsibility cultivated during a time of significant social change. Many witnessed firsthand the impact of both positive and negative social movements and have a strong desire to contribute to positive change. Furthermore, a desire to leave a legacy, both within their families and the broader community, is a powerful motivator.

This legacy isn’t solely defined by financial wealth but also by the positive impact they’ve had on the world. Finally, many Baby Boomers are driven by a personal connection to the causes they support, often stemming from personal experiences or the experiences of loved ones. This personal connection fuels a deep commitment and consistent support.

Examples of Baby Boomer Supported Initiatives

Baby Boomers have consistently supported a wide range of charitable causes. Examples include significant contributions to educational institutions, particularly those focused on higher education and research. They have also heavily supported medical research, particularly cancer research and organizations addressing diseases prevalent amongst their age group. Environmental conservation efforts have also attracted substantial support, reflecting a growing awareness of environmental issues.

Finally, many Baby Boomers actively contribute to organizations focused on supporting veterans and military families, stemming from their experiences during the Vietnam War and other conflicts. These are just a few examples illustrating the diversity of causes supported by this generation.

Methods of Charitable Giving Among Baby Boomers

The ways in which Baby Boomers contribute to charitable causes are diverse and reflect their individual values and circumstances.

- Direct Donations: Many Baby Boomers make direct monetary donations to charities they support, either through one-time gifts or recurring contributions.

- Planned Giving: A significant portion engages in planned giving, such as bequeathing assets to charities in their wills or establishing charitable trusts.

- Volunteer Work: Many Baby Boomers actively volunteer their time and skills to the organizations they support, contributing valuable expertise and manpower.

- In-Kind Donations: They often donate goods, such as clothing, food, or household items, to local charities and shelters.

- Matching Gifts: Some actively participate in matching gift programs offered by their employers, effectively doubling their contributions.

- Endowment Contributions: Many contribute to endowments, ensuring long-term financial support for institutions and causes they believe in.

So, are Baby Boomers stingy? The answer, as we’ve seen, is far more nuanced than a simple yes or no. Their financial habits are a complex tapestry woven from historical events, personal experiences, and evolving priorities. While some may appear frugal, their financial prudence often stems from a lifetime of navigating economic uncertainty and prioritizing long-term security. Understanding their perspective allows us to move beyond simplistic stereotypes and appreciate the multifaceted realities of generational wealth and spending.